Banking integrations are no longer just about connecting financial institutions to payment processors. Today, banks are embedding their services into retail, e-commerce, telecom, and fintech ecosystems, requiring secure, high-performance, and flexible integrations that can handle millions of transactions daily.

Yet, many banks still struggle with failed integrations, poor scalability, and compliance issues. Why? Because successful banking integrations require more than just technical execution—they demand strategic planning, security-first architecture, and future-proof scalability.

At 42Flows, we have spent over seven years delivering real-world banking integrations, working with payment providers, retailers, and digital-first financial institutions. This article shares key lessons learned, common pitfalls to avoid, and best practices for ensuring a seamless banking integration.

A banking integration is only successful if it solves real business problems. Many failures happen when banks start integrating without a clear roadmap.

Lesson Learned: The most successful integrations start with a clear scope and a roadmap, avoiding unnecessary complexity.

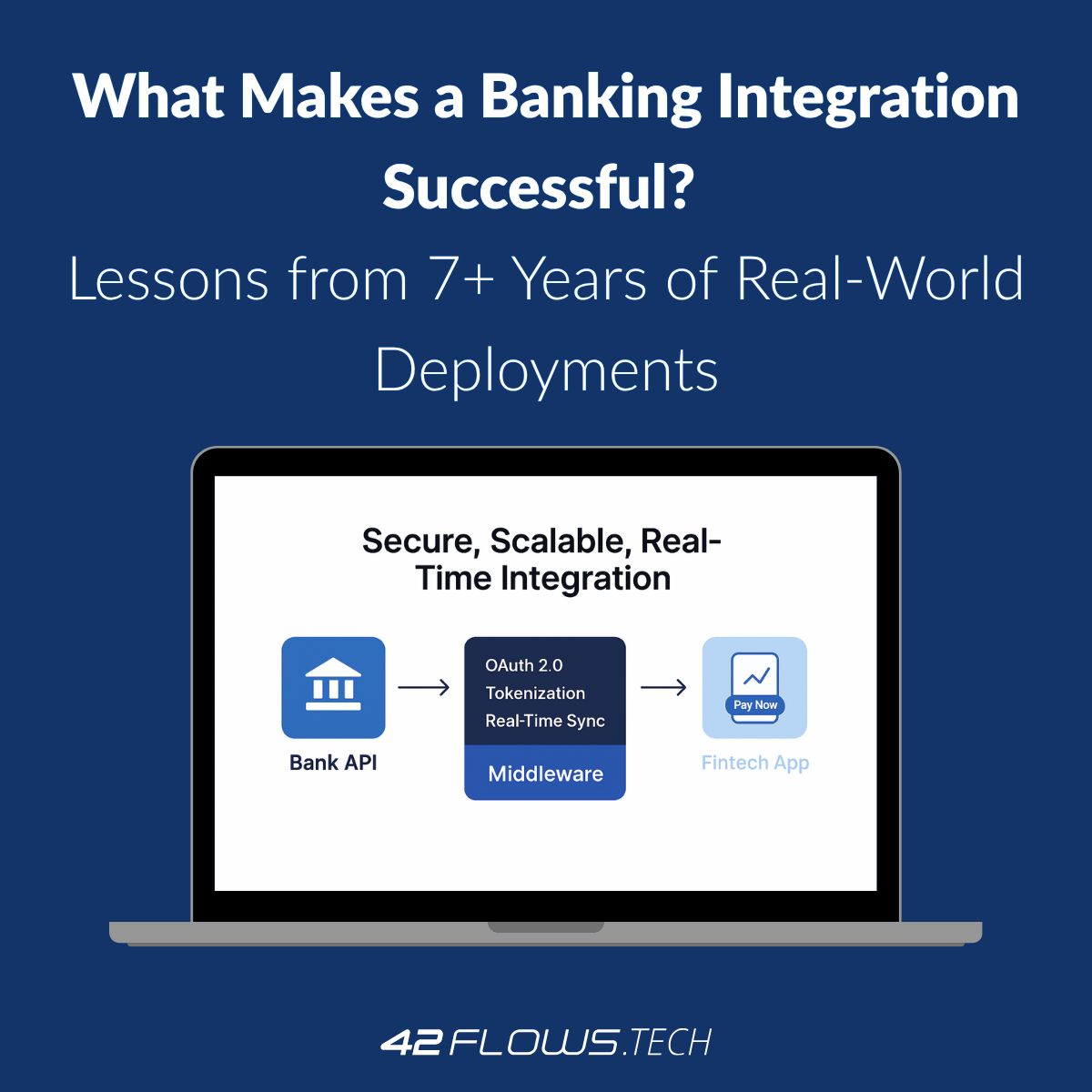

Banking integrations are a prime target for fraud, data breaches, and cyberattacks. Security should be part of the design process, not an add-on.

Lesson Learned: A security-first approach prevents compliance issues and cyber risks before they become major problems.

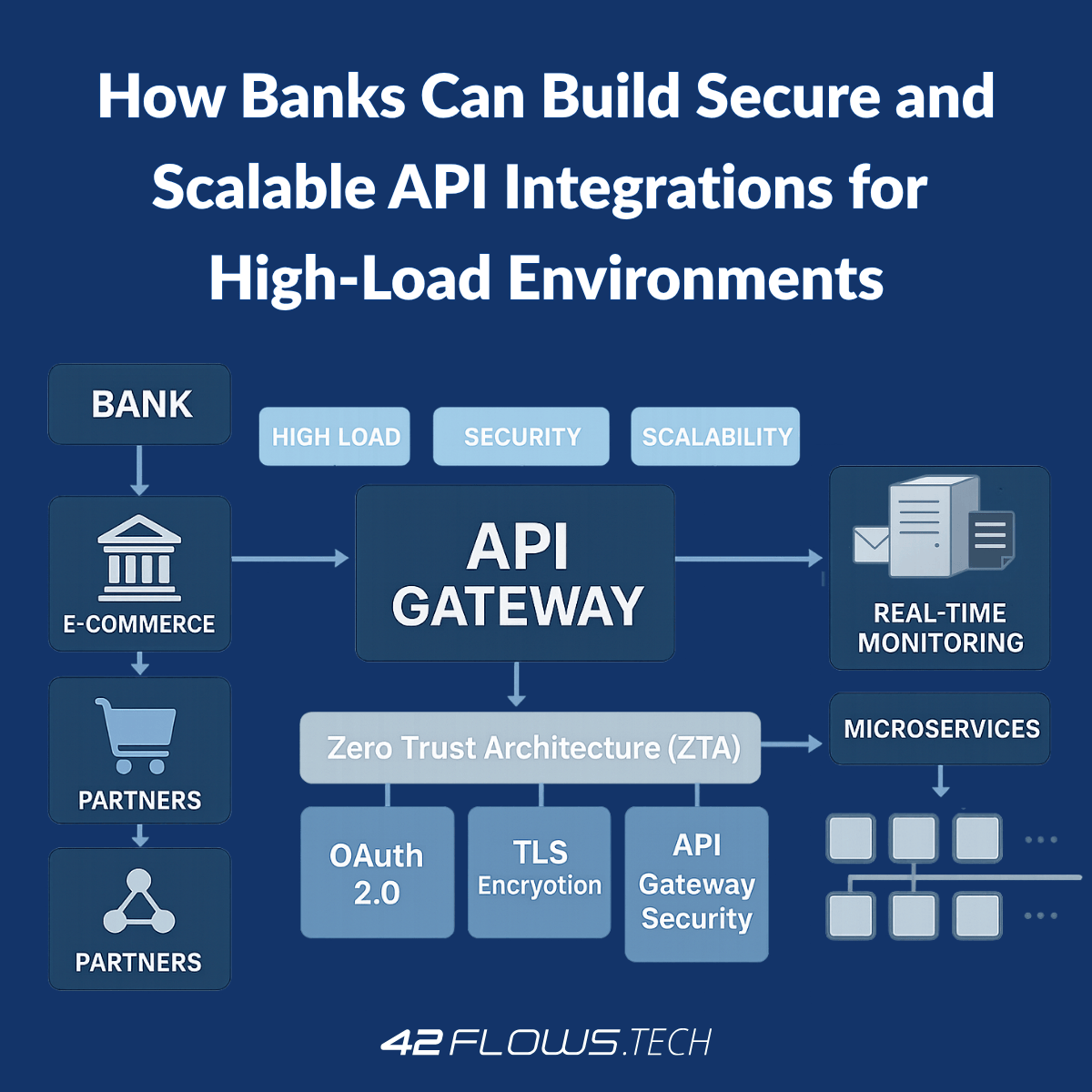

Many banking integrations fail due to performance bottlenecks during peak usage. The key is to design APIs that scale dynamically.

Case Study: A retail bank integrated with an e-commerce giant, but their monolithic API structure caused failures during peak sales events. After switching to microservices and dynamic scaling, they improved uptime to 99.99 percent.

Lesson Learned: If an API cannot scale, the integration will fail when transaction volumes spike.

Many banking integrations fail because data is not synced in real time, leading to delays in payments, incorrect balances, or missing transactions.

Lesson Learned: Real-time data syncing is critical for smooth banking operations.

Banks that only test in controlled environments risk integration failures when launched. The best integrations go through stress testing, failure simulations, and real-world scenario testing.

Lesson Learned: Pre-launch testing must simulate real-world banking usage, not just ideal conditions.

Many banks still operate on monolithic, outdated infrastructure, making modern API integrations difficult.

Solution:

Not all banks, retailers, or fintech partners use the same API formats or security protocols.

Solution:

A global banking integration must comply with varying security, privacy, and financial regulations.

Solution:

Looking ahead, successful banking integrations will need to adapt to:

Banks that stay ahead of these trends will gain a competitive advantage in offering seamless, next-generation financial services.

After seven years of deploying banking integrations, one thing is clear: successful integrations do not just “connect” systems—they enhance security, efficiency, and customer experience.

The key lessons from our experience:

At 42Flows, we specialize in seamless, secure, and scalable banking integrations that connect financial institutions with retailers, fintechs, and telecom providers.

Let’s talk. Just enter your details and we will reply within 24 hours.

Maksym Popov

Maksym Popov